5 Year anniversary of the Rivers portfolios.

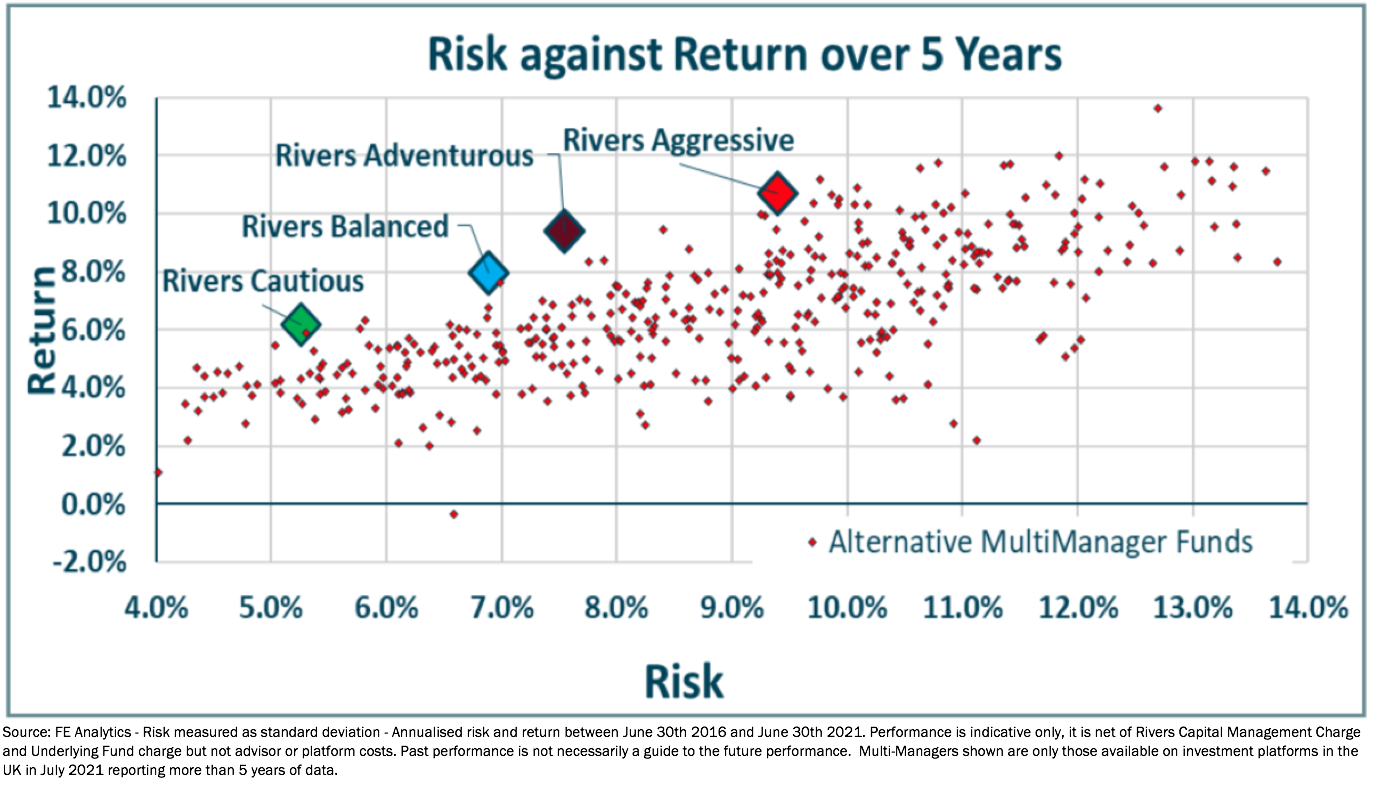

The end of June marked 5 years since Rivers launched its risk rated Model Portfolios on Platforms on June 30th 2016. While the scope since then has included the introduction of offshore and ESG portfolios (June 2017) as well as a number of tailored solutions the process has changed little since launch. Our objective then was, and still remains, to build portfolios using sets of diversified funds, combining both passive and active strategies. The Rivers tactical asset allocation strategy systematically adjusts those portfolios to align with the relative risk level, or attractiveness, of the global investment market according to our Risk Committee view. Given this anniversary, in this Focus piece we look back on the relative performance of that strategy. We are delighted to report that all targets have been met in terms of both risk and return. We are perhaps even more delighted to report that, on a risk adjusted basis, we can show that these unbundled model portfolios have outperformed very nearly all listed multimanager fund solutions, after all costs, over the last five years. Alongside this delight however we want to focus on how this performance was achieved, particularly given that, over 5 years of generally positive asset class value growth, the Risk Committee has maintained, for the large part, an underweight risk allocation. For much of the last five years the Risk Committee has held, and currently hold, a belief that asset valuations are unsustainably high.

Our Global View

We have always tried to take a global view on investment. Since our first Risk Committee meeting in 2016, in the aftermath of the UK Referendum which led to Brexit, we’ve tried to view the investment portfolios within the global context. The election of President Trump, whatever our views on him personally, was always likely to influence global economic growth more than Brexit. Despite Trump’s issues with China they affected asset prices less than we expected. His domestic policies, especially on tax, boosted the profitability of US companies, and equity markets, more than we expected. Similarly the Federal Reserve, raising rates in late 2018, impacted asset prices less than we expected, and cutting rates so quickly, in early 2020, with the backing of aggressive fiscal intervention, boosted valuations for longer than we had expected. Our risk committee was correctly positioned for all of these calls but we were often too early in and often out too soon. Sometimes both. Tactical changes have added to our performance. adding risk during the falls of late 2018 and early 2020 has added value, but it is difficult to conclude that a generally underweight risk position over the last five years will have added value.

Adding Risk

Objectively speaking the ability to add risk when it gets cheaper has added value, occasionally a lot, but that is not the biggest contributor to the success of the portfolios we manage. It has been diversification that have been key to the portfolio success at Rivers. By including Diversifiers into the portfolio allocation, which are investments with a low correlation to equity and Interest rate risks, it has been possible to add value overall while reducing losses during the few market falls that the markets have experienced.

Portfolio Construction vs Market Timing

The last 5 years, and in fact the last 12 years in reality, have been a time when a simple investment strategy of buying equity risk and adding interest rate risk (to lower overall risk) should have been successful. Over that period Equity indices have seen valuations increase to an astonishing degree. Mega-cap stocks have outperformed and interest rates, over the 5 years have gone from low to non-existent or even negative. In such an environment, adding value as active fund managers has been difficult. The only way to keep up has been market timing, which is difficult, or by the use of efficient portfolio construction. The fact that the Rivers portfolios have not only kept up with but exceeded, on a risk adjusted basis, all the multimanager funds available, passive or active, is primarily a result of efficient portfolio construction. With the wonderful benefit of hindsight it is fair to say the portfolios’ tactical positioning, while having allowed the adding of risk during market sell offs, has not taken full advantage of the opportunity.

Difficult environment for passive strategies

As always with investment the tide changes. Price earnings multiples will not rise forever, inflation will rise, as will interest rates. We are not suggesting any of these economic certainties will make it easier for Rivers portfolios to perform but we do think it will make it a lot harder for passive, market capitalisation led strategies to do well. The lack of Diversifiers in such an environment will make portfolio performance even more difficult.

Overvalued Markets?

If, as we currently believe, the US market reaches a level beyond which even the most optimistic investor asks questions followed by a period of multiple “re-rating” then a pure equity and bond market approach is very likely to struggle. A diversified strategy, all other things being equal, will fare better. On a relative basis we expect a tactical diversified portfolio strategy will find it easier to outperform over the coming five years than it has over the last five years. If we are wrong, and the market continues to rise indefinitely, then we remain confident the Rivers portfolios will continue to meet their objectives.