This website is for the use of authorised and regulated financial advisers, and is not suitable for, or to be relied upon by, other investors. If you are a retail investor please take advice from your financial adviser. By proceeding to the website please note that you will be treated as a professional adviser for regulatory purposes. The Website is for information purposes only and does not constitute investment advice; any information is subject to change without notice. The Information is not directed at any person or entity. The Information is intended only for use by users domiciled in the United Kingdom and is not intended for distribution or use in any jurisdiction or country where it is illegal or unlawful to access and use such information. Non-UK investors should consider their local regulations before considering investment. The use of the Website is at your own personal risk.

Rivers Capital Management is authorised and regulated by the Financial Conduct Authority (FCA number 801238)

Every portfolio is built around stated investment plan with a target level return to be achieved within risk and a maximum loss constraints. Portfolios start with a robust Long-term Strategic Asset Allocation that will determine risk characteristics more than any other factor.

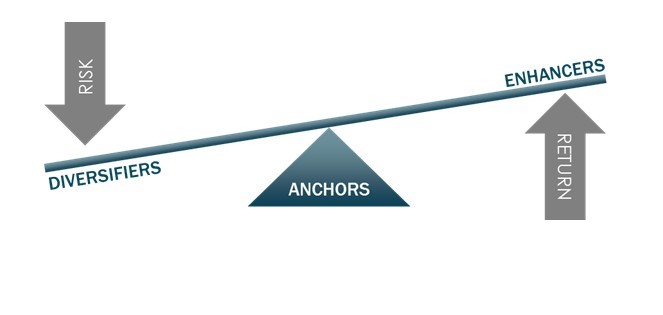

Studies have shown that as much as 80% of the overall long term return and risk of a portfolio comes from the long-term strategic asset allocation. In that regard we think the traditional Bonds-Equity-Alternative investment categories fail to adequately account for the changing investment landscape. Given the vast proliferation of complex investment strategies in recent years we believe this ‘Asset Class’ based portfolio construction methodology to be outdated and can lead to unknowingly excessive risk. At Rivers, we adopt the categories of ‘Anchor’, ’Enhancer’ and ‘Diversifier’ in order to take into account the wider range of risk available in asset classes and to ensure that strategic portfolios are focused on more relevant risk criteria.

Step 1: Anchors

Historically where Cash and Bond assets have been used to build a core of low volatility investments, we prefer to begin our process by designing what we can “Anchor” to the portfolio. Assets which “Anchor” the portfolio do include traditional Fixed Income instruments, but only those with very high credit quality. Anchor assets can also be found in certain Low Risk absolute return opportunities although liquidity often prevents inclusion. Essentially “Anchor” investments are selected for low market correlation, low risk and capital preservation.

Step 2: Enhancers

Where higher returns are required and risk can be increased we would add “Enhancer” Assets to the portfolio by adding equity related risk. Enhancer assets can be direct equity, public equity or credit with a high correlation to equity growth. Enhancer assets should offer long term attractive returns but with higher short and medium term capital risk and volatility. Enhancers will generally follow economic and market trends and need to be moderated for portfolios with limited maximum loss constraints.

Step 3: Diversifiers

These include commodity investments, macro timing funds, uncorrelated credit funds, real estate and other market neutral uncorrelated funds. The individual volatility of these investments is less important than the minimal or negative correlation to either interest rate or equity market risk. These assets often have high positive returns but their inclusion is primarily to diversify risk and therefore the non-correlation is the primary driver.

The Anchor, Enhancer and Diversifier asset categories are then divided into secondary asset classes which more closely align with traditional investment benchmarks and capital markets. At Rivers Capital Management we compute forward-looking asset class return estimates using the mathematical model developed by Fischer Black and Robert Litterman and published in 1992. This model essentially improves modern portfolio theory by providing accurate estimates for returns that are based more on diversification and levels of risk than historical analysis.

The process produces three types of results:

‘Equilibrium Returns’, or long-term returns, for each asset class.

‘Equilibrium Volatility’, or long-term volatility, for each asset class.

‘Equilibrium Correlation Matrix’, or long-term correlations for all asset classes.

By using risk related categorisation and by monitoring the correlation between investments we are seeking to create efficient diversified portfolios. These portfolios are adapted and managed using this process while ensuring that our objective remains that portfolios stay within pre-determined and controlled levels of risk.

Read more about our processes hereBack

Step 1: Anchors

Historically where Cash and Bond assets have been used to build a core of low volatility investments, we prefer to begin our process by designing what we can “Anchor” to the portfolio. Assets which “Anchor” the portfolio do include traditional Fixed Income instruments, but only those with very high credit quality. Anchor assets can also be found in certain Low Risk absolute return opportunities although liquidity often prevents inclusion. Essentially “Anchor” investments are selected for low market correlation, low risk and capital preservation.

Step 2: Enhancers

Where higher returns are required and risk can be increased we would add “Enhancer” Assets to the portfolio by adding equity related risk. Enhancer assets can be direct equity, public equity or credit with a high correlation to equity growth. Enhancer assets should offer long term attractive returns but with higher short and medium term capital risk and volatility. Enhancers will generally follow economic and market trends and need to be moderated for portfolios with limited maximum loss constraints.

Step 3: Diversifiers

These include commodity investments, macro timing funds, uncorrelated credit funds, real estate and other market neutral uncorrelated funds. The individual volatility of these investments is less important than the minimal or negative correlation to either interest rate or equity market risk. These assets often have high positive returns but their inclusion is primarily to diversify risk and therefore the non-correlation is the primary driver.

The Anchor, Enhancer and Diversifier asset categories are then divided into secondary asset classes which more closely align with traditional investment benchmarks and capital markets. At Rivers Capital Management we compute forward-looking asset class return estimates using the mathematical model developed by Fischer Black and Robert Litterman and published in 1992. This model essentially improves modern portfolio theory by providing accurate estimates for returns that are based more on diversification and levels of risk than historical analysis.

The process produces three types of results:

‘Equilibrium Returns’, or long-term returns, for each asset class.

‘Equilibrium Volatility’, or long-term volatility, for each asset class.

‘Equilibrium Correlation Matrix’, or long-term correlations for all asset classes.

By using risk related categorisation and by monitoring the correlation between investments we are seeking to create efficient diversified portfolios. These portfolios are adapted and managed using this process while ensuring that our objective remains that portfolios stay within pre-determined and controlled levels of risk.

Step 1: Anchors

Historically where Cash and Bond assets have been used to build a core of low volatility investments, we prefer to begin our process by designing what we can “Anchor” to the portfolio. Assets which “Anchor” the portfolio do include traditional Fixed Income instruments, but only those with very high credit quality. Anchor assets can also be found in certain Low Risk absolute return opportunities although liquidity often prevents inclusion. Essentially “Anchor” investments are selected for low market correlation, low risk and capital preservation.

Step 2: Enhancers

Where higher returns are required and risk can be increased we would add “Enhancer” Assets to the portfolio by adding equity related risk. Enhancer assets can be direct equity, public equity or credit with a high correlation to equity growth. Enhancer assets should offer long term attractive returns but with higher short and medium term capital risk and volatility. Enhancers will generally follow economic and market trends and need to be moderated for portfolios with limited maximum loss constraints.

Step 3: Diversifiers

These include commodity investments, macro timing funds, uncorrelated credit funds, real estate and other market neutral uncorrelated funds. The individual volatility of these investments is less important than the minimal or negative correlation to either interest rate or equity market risk. These assets often have high positive returns but their inclusion is primarily to diversify risk and therefore the non-correlation is the primary driver.

The Anchor, Enhancer and Diversifier asset categories are then divided into secondary asset classes which more closely align with traditional investment benchmarks and capital markets. At Rivers Capital Management we compute forward-looking asset class return estimates using the mathematical model developed by Fischer Black and Robert Litterman and published in 1992. This model essentially improves modern portfolio theory by providing accurate estimates for returns that are based more on diversification and levels of risk than historical analysis.

The process produces three types of results:

‘Equilibrium Returns’, or long-term returns, for each asset class.

‘Equilibrium Volatility’, or long-term volatility, for each asset class.

‘Equilibrium Correlation Matrix’, or long-term correlations for all asset classes.

By using risk related categorisation and by monitoring the correlation between investments we are seeking to create efficient diversified portfolios. These portfolios are adapted and managed using this process while ensuring that our objective remains that portfolios stay within pre-determined and controlled levels of risk.