Welcome to the Rivers Capital Management website.

This website is for the use of authorised and regulated financial advisers, and is not suitable for, or to be relied upon by, other investors. If you are a retail investor please take advice from your financial adviser. By proceeding to the website please note that you will be treated as a professional adviser for regulatory purposes. The Website is for information purposes only and does not constitute investment advice; any information is subject to change without notice. The Information is not directed at any person or entity. The Information is intended only for use by users domiciled in the United Kingdom and is not intended for distribution or use in any jurisdiction or country where it is illegal or unlawful to access and use such information. Non-UK investors should consider their local regulations before considering investment. The use of the Website is at your own personal risk.

Rivers Capital Management is authorised and regulated by the Financial Conduct Authority (FCA number 801238)

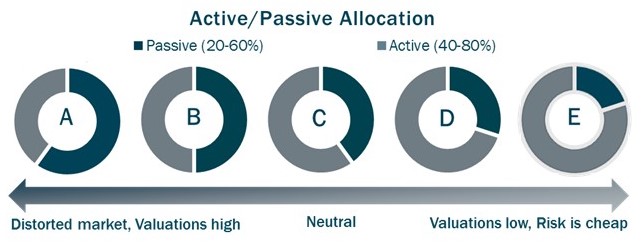

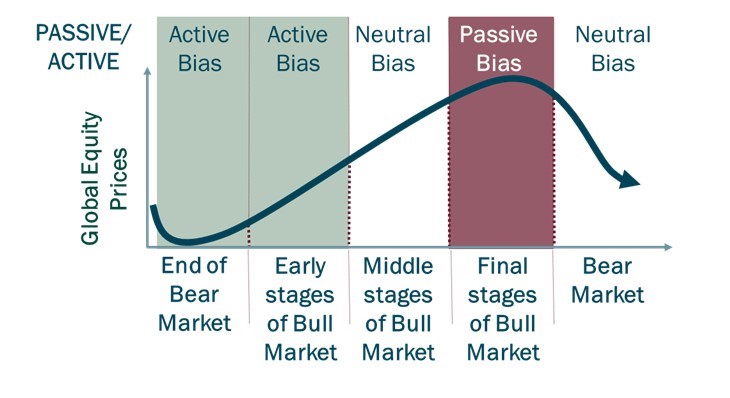

At Rivers we don't pretend we have the foresight to predict the exact tipping point or market inflection points, but we do believe that if assets, or markets are expensive we should reduce overall risk. Our statistical research tells us that during those periods of distortion when corrections are delayed and prices continue to get more ‘irrationally’ expensive, passive strategies will likely perform strongly. Risk reduction is, therefore, implemented by reducing the exposure to active strategies. The portfolios will, therefore, likely be underweight risk and overweight passives. Our research demonstrates that with this strategy the portfolio is likely to sustain target returns during periods of ‘irrational exuberance’ despite often being overall under exposed to market risk.

Once these distortions have corrected sufficiently and prices have reverted back to normality or indeed have become compellingly cheap, we believe it is appropriate to add risk to a portfolio. This risk should be added through active managers who throughout falling markets or at the start of a recovery or new bull market cycle tend to do well relative to their passive benchmarks.

In a neutral investment environment where risk is average, we would expect the allocation between active and passive to be 60:40. In periods of low risk the maximum active allocation, within the cost constraints agreed on the portfolio, would be 80%, with 20% in passives. During periods of price distortion we would expect the passive allocation to be as high as 60% with actives as low as 40%.

The current Flexible Active/Passive Allocation is articulated in published monthly factsheets and the Rivers Capital Management newsletter ‘Current Focus’.

At Rivers we don't pretend we have the foresight to predict the exact tipping point or market inflection points, but we do believe that if assets, or markets are expensive we should reduce overall risk. Our statistical research tells us that during those periods of distortion when corrections are delayed and prices continue to get more ‘irrationally’ expensive, passive strategies will likely perform strongly. Risk reduction is, therefore, implemented by reducing the exposure to active strategies. The portfolios will, therefore, likely be underweight risk and overweight passives. Our research demonstrates that with this strategy the portfolio is likely to sustain target returns during periods of ‘irrational exuberance’ despite often being overall under exposed to market risk.

Once these distortions have corrected sufficiently and prices have reverted back to normality or indeed have become compellingly cheap, we believe it is appropriate to add risk to a portfolio. This risk should be added through active managers who throughout falling markets or at the start of a recovery or new bull market cycle tend to do well relative to their passive benchmarks.

In a neutral investment environment where risk is average, we would expect the allocation between active and passive to be 60:40. In periods of low risk the maximum active allocation, within the cost constraints agreed on the portfolio, would be 80%, with 20% in passives. During periods of price distortion we would expect the passive allocation to be as high as 60% with actives as low as 40%.

The current Flexible Active/Passive Allocation is articulated in published monthly factsheets and the Rivers Capital Management newsletter ‘Current Focus’.